When to Form an LLC for Your DTF Business

Aug 17, 2025 (Updated on Oct 28, 2025)

So, your passion for creating vibrant, high-quality DTF (Direct-to-Film) transfers has blossomed from a side hustle into a thriving business. The orders are rolling in, your designs are getting noticed, and you're starting to see some real financial growth. First of all, congratulations! That's a huge accomplishment. But with great growth comes great responsibility—and some important business decisions.

One of the most critical decisions you'll face is when to transition your business structure from a sole proprietorship to a Limited Liability Company (LLC). It’s a question that many creative entrepreneurs grapple with, and for good reason. The structure of your business has significant implications for your personal liability, taxes, and overall scalability. This guide will walk you through the key financial and operational indicators that signal it might be time to make the switch for your growing DTF business.

Understanding the Core Difference: Sole Proprietorship vs. LLC

At its heart, the choice comes down to one critical factor: the legal line between your business finances and your personal ones. In a sole proprietorship, that line doesn't exist, meaning your personal assets are legally tied to the business's fate. An LLC, on the other hand, intentionally draws that line, creating a protective shield that is essential for safeguarding your personal wealth as you grow. Before we dive into the "when," let's quickly clarify the "what."

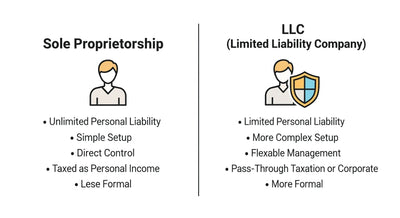

The Sole Proprietorship: The Simple Start

A sole proprietorship is the most straightforward business structure. The beauty of this model is its ease of entry; you have complete control, and all profits and losses are simply reported on your personal tax return. This keeps accounting straightforward in the early days when you are focused on perfecting your craft and building a customer base. The critical trade-off for this simplicity, however, is that you are personally liable for all business debts and legal actions, putting your personal assets at risk. If you're running your DTF business on your own and haven't formally registered it as anything else, you're likely a sole proprietor.

- Pros: Easy and inexpensive to set up (you basically just start doing business), complete control, and simple tax filing (you report business income on your personal tax return).

- Cons: The biggest drawback is the lack of personal liability protection. You and your business are legally the same entity. This means if your business incurs debt or is sued, your personal assets—like your car, house, and personal savings—are at risk.

The LLC: A Shield for Your Assets

An LLC is a hybrid business structure that combines the pass-through taxation of a sole proprietorship with the limited liability of a corporation.

- Pros: It creates a legal barrier between your personal assets and your business debts. This "corporate veil" is the primary reason many business owners choose to form an LLC. It also offers more credibility to clients and suppliers and provides more flexibility in how you're taxed.

- Cons: It's more complex and costly to set up and maintain than a sole proprietorship, requiring registration fees and potentially annual reporting.

Financial Signs It’s Time to Form an LLC

Its most powerful feature is the creation of a "corporate veil," which legally separates your personal assets from your business's debts and liabilities. This formal structure instantly boosts your business's credibility, making it appear more professional to clients, suppliers, and potential lenders. Ultimately, this shield gives you the freedom to grow your business with the invaluable peace of mind that your personal wealth is protected.How do you know when the risks of a sole proprietorship outweigh its simplicity? Here are the key financial and operational signals to watch for.

1.Your Business Is Generating Significant Revenue

There's no magic number, but a common milestone is when your business's income becomes a substantial part of your personal income. As your revenue grows, so does your potential liability. A lawsuit that might have seemed minor when you were making a few hundred dollars a month can be devastating when your business is clearing thousands.

Think About it This Way: the more money your business makes, the more you have to lose. Forming an LLC protects your personal savings and assets from business-related legal issues. This is especially important in the custom apparel industry, where issues like copyright infringement or customer disputes over large orders can arise.

2.You're Taking on Business Debt

Are you planning to take out a business loan to buy a new, high-capacity printer? Or perhaps you're using a business credit card to purchase a larger stock of high-quality films and powders for your dtf transfers.

When you take on debt as a sole proprietor, you are personally guaranteeing that debt. If the business fails and can't repay the loan, creditors can come after your personal assets. An LLC, on the other hand, can take on debt in its own name. While some lenders may still require a personal guarantee, forming an LLC is a crucial first step in separating your business and personal finances and can make securing funding easier in the long run.

3.You're Hiring Employees or Contractors

This is a major turning point for any small business. The moment you bring someone else on board, whether as a full-time employee or a regular contractor, your liability skyrockets. You're now responsible for payroll, workplace safety, and the actions of your employees while they are on the job.

Imagine an employee gets injured while operating your heat press, or a contractor makes a mistake that ruins a major client's order. As a sole proprietor, you are personally on the hook for those liabilities. An LLC helps shield you from personal responsibility for these types of incidents, making it an almost essential step before you start building your team.

4.You're Signing Major Contracts or Leases

Is your DTF business growing to the point where you need to lease a commercial space? Or are you signing a long-term contract with a major apparel brand to be their exclusive provider of dtf transfers?

These are exciting steps, but they also come with significant legal and financial commitments. If you sign a commercial lease as a sole proprietor and your business can no longer afford the rent, the landlord can sue you personally for the remainder of the lease term. By having an LLC as the signatory on the contract, you ensure that the business entity, not you personally, is responsible for fulfilling the terms. This adds a layer of professionalism and protection that is critical when dealing with high-stakes agreements.

5.Your Tax Situation is Becoming More Complex

While a sole proprietorship offers simple tax filing, an LLC provides more flexibility. By default, a single-member LLC is taxed like a sole proprietorship (a "disregarded entity"). However, an LLC can also elect to be taxed as an S-Corporation.

This can lead to significant tax savings once your business reaches a certain level of profitability. With an S-Corp election, you can pay yourself a "reasonable salary" and take the remaining profits as distributions. Salary income is subject to self-employment taxes (Social Security and Medicare), but distributions are not. This can save you a substantial amount in taxes each year, often more than enough to cover the costs of forming and maintaining the LLC. It's a good idea to speak with an accountant to see if this strategy is right for your financial situation.

Making the Leap: Your Next Steps

If you're nodding your head in agreement with several of the points above, it’s likely time to start the process of forming an LLC. While it might seem daunting, it's a manageable process. The core of this transition involves filing official paperwork, known as Articles of Organization, with your state to legally establish your company as a separate entity. Once registered, you will need to obtain an Employer Identification Number (EIN) from the IRS, which is essential for opening a business bank account and hiring employees. Finally, creating an internal operating agreement will set the rules for how your business runs, solidifying a professional foundation that protects your personal assets.

- Choose a Business Name: Make sure the name you want is available in your state and complies with its naming rules.

- File Articles of Organization: This is the official document you file with the state to formally create your LLC.

- Appoint a Registered Agent: This is a person or service designated to receive official legal and government correspondence on behalf of your business.

- Create an Operating Agreement: While not required in all states, this internal document outlines how your LLC will be run. It’s highly recommended.

- Obtain an EIN: You'll need an Employer Identification Number from the IRS to open a business bank account and hire employees.

While you can do this yourself, many business owners choose to use an online legal service or consult with an attorney to ensure everything is done correctly.

For a local business looking to establish itself, having a solid legal foundation is just as important as having the best equipment. When you're ready to scale, you want to know that your personal finances are secure. Companies like DTF Dallas understand the importance of a professional and reliable operation, and forming an LLC is a key part of building that trust and stability in the local small business ecosystem.

💬 Your Top LLC Questions, Answered

-

Q: Can I pay myself from my LLC?

- A: Yes. How you pay yourself depends on how your LLC is taxed. If it's a "disregarded entity," you take owner's draws. If you elect to be taxed as an S-Corp, you'll pay yourself a formal salary and can also take distributions of profits.

-

Q: How much does it cost to form an LLC?

- A: The cost varies by state. You'll have a one-time filing fee that can range from $50 to $500, and some states also require an annual report fee to keep your LLC in good standing.

-

Q: Do I need a separate bank account for my LLC?

- A: Absolutely. This is crucial for maintaining the liability protection of the LLC. Mixing personal and business funds (known as "co-mingling") can "pierce the corporate veil," putting your personal assets at risk in a lawsuit.

-

Q: Can I still be held personally liable for anything with an LLC?

- A: Yes. The liability shield isn't absolute. You can still be held personally liable for things like personal guarantees on loans, professional malpractice, or personally injuring someone. However, it protects you from general business debts and the actions of your employees.

Explore our premium dtf transfers today and see why so many growing businesses trust DTF Dallas for their printing needs!

Comments 0

Be the first to leave a comment.